Water’s welling up from your apartment floor and you’re sure your water pipes aren’t the culprit – so who’s liable?

Drip. drip. Waking up to the sound of water, you see puddles form on the floor. Perhaps it was a burst pipe or some plumbing issue. Whatever the cause, you’re pretty sure the water damage isn’t your fault – but who is liable? Is HOA responsible for water damage?

If you’re the unit owner of a townhouse or condominium in a housing development, which kind of water damage falls under property management, and for which should you file an insurance claim?

When is your Homeowners Association (HOA) responsible for water damage? It all depends on the source and location of the water damage and the specific rules outlined in your HOA‘s governing documents.

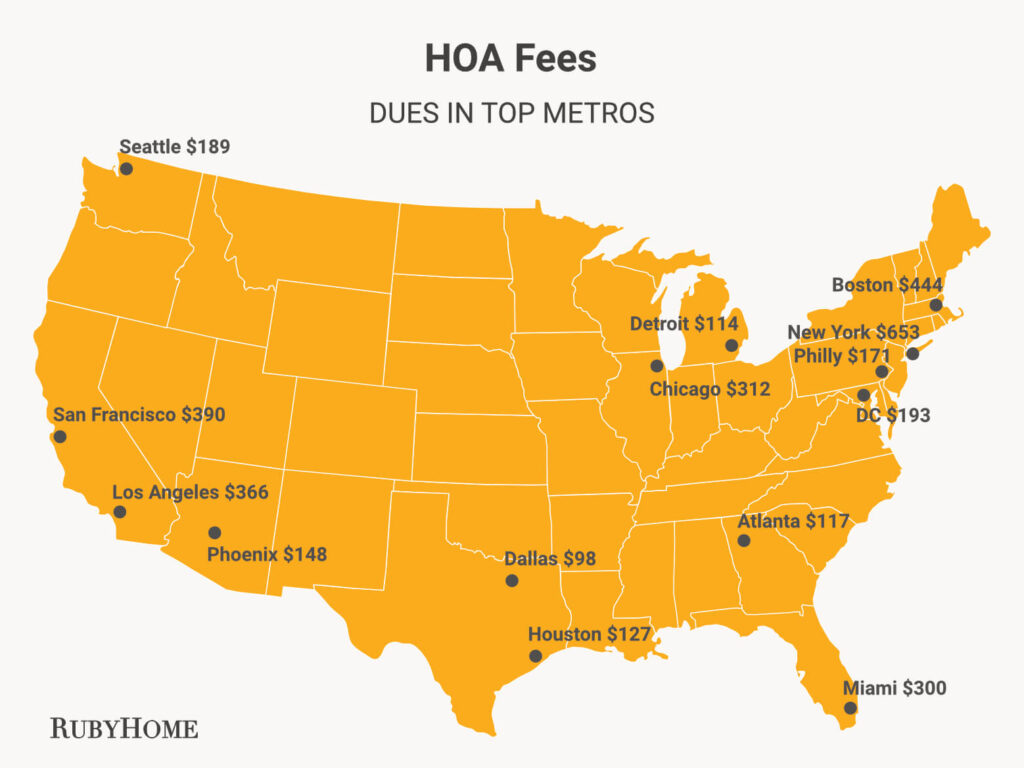

The state of New York had little over 14,000 HOAs in 2022, with roughly 1.4 million homes and 13% of New York’s homeowners represented in those HOA communities.

For those homeowners, their respective Homeowner Association plays an important part in the organization and management of their residential community. In case of water damage, your HOA may take responsibility. Given that average HOA fees in New York are the highest in the country, as one real estate company estimated, you’d certainly hope so.

Source: RubyHome Luxury Real Estate

Before anyone starts pointing fingers, homeowners should understand their HOA’s responsibilities regarding water damage.

If you don’t know who’s liable, you might end up footing a big bill that the community association or your insurance policy would have covered. Knowing where your and your HOA’s responsibilities start and end prevents disputes with your neighbors and condo association over who should take action.

Let’s break down where HOAs may or may not be responsible for water damage in New York.

In this article, we explain the main factors to take into consideration when determining liability:

- Governing documents

- Sources of water damage

- Insurance policies and responsibilities

With all aspects of both owners and their HOA’s responsibility explained, we then provide a 7-step guide to determining liability and filing an insurance claim for water damage.

So when is HOA responsible for water damage? Read on to find out.

[Water damage requires immediate response. Call Lux Restoration to have our emergency water remediation crew on your doorstep in 60 minutes.]

Consulting HOA’s governing documents

A water leak is rarely just a pipe in need of fixing. If not treated directly, water finds its way into your drywalls and foundations, causing serious property damage. What’s more, the repair costs can leave a gaping hole in your wallet.

But don’t start paying any bills just yet – those leaking water pipes might not be your fault. Who should have taken care of that plumbing issue in the first place? Likely the Homeowners Association.

Want to know when your HOA is responsible for water damage? Always check the governing documents.

HOA documents contain the following paperwork: the Covenants, Conditions, and Restrictions (referred to as the CC&Rs), bylaws, and rules and regulations. These documents together define the rights and responsibilities of the individual unit owner and the association.

The CC&Rs should tell you who’s liable for water damage and under which circumstances. Does HOA cover plumbing? It’s somewhere in the CC&Rs. Is HOA responsible for roof leaks? Again, consult the CC&Rs.

As a rule of thumb, though, HOA is responsible for exterior water damage, while interior damage is the owner’s responsibility.

Common areas vs owner responsibility

Also outlined in the association’s governing documents is the delineation between private and common areas. The CC&Rs should contain a detailed outline of where these boundaries lie.

The CC&Rs can further distinguish between general common areas and limited common areas, sometimes also called exclusive use common areas.

Common areas (or common elements) are designed to be used by everyone. These are maintained by the HOA management company or its contractors. Limited common areas refer to elements that are limited to use by one or some unit owners but not all owners in the community.

Specifics of who is responsible for the maintenance and upkeep of limited common elements are outlined in the CC&Rs and sometimes in the bylaws.

The division between common elements and individual units (also referred to as separate interests) helps determine water damage liability.

Let’s say that the lobby or hallway has water damage due to leaky pipes. If the CC&Rs state that the condo association is responsible for maintaining utilities in the common areas, it’s more than likely that they’re the ones responsible for the water damage restoration.

But when water pipes within the limits of an individual condo unit cause water damage due to wear and tear, that’s the owner’s responsibility.

But what if it wasn’t regular wear and tear? If that plumbing issue arises due to negligence of HOA management, where an unserviced plumbing system caused a burst pipe in an individual unit, any water damage to personal property is the Homeowner Association’s responsibility.

Cases of water damage where it’s not immediately clear where the ultimate responsibility lies happen frequently. Whenever you’re unsure who bears liability for the repairs, it helps to logically and calmly assess the situation.

7 Steps to Determine Liability for Water Damage

To properly determine water damage liability in a housing development or condominium governed by a Homeowners Association, follow the 7 steps below to find the responsible party and file a claim:

| Step | Action |

| 1 | Identify the Source of the Water Damage: – Plumbing issues (burst pipes, water heater leaks, clogged drains) – Roof leaks – Storms and flooding – Appliance leaks (washing machines, HVAC systems, sewage backups) |

| 2 | Determine the Location of the Damage: – Common areas (lobbies, hallways, amenities) maintained by HOA – Limited common areas for use by some unit owners – Inside an individual unit or home |

| 3 | Review HOA‘s Governing Documents: – Consult the CC&Rs, bylaws, and rules & regulations – Look for delineation of boundaries between common and private areas – Check for specific clauses about water damage responsibility |

| 4 | Consider Negligence and Maintenance Factors: – Was there negligence by your HOA in maintaining common utilities? – Did the unit owner fail to properly maintain their individual property? – Who was responsible for the area where the issue originated? |

| 5 | Understand Insurance Policies: – HOA‘s master policy covers common areas and may have deductibles – Homeowner’s individual policy covers interior units and belongings – Policy details determine coverage for different water damage causes |

| 6 | Determine Liability: – Based on source, location, governing docs, negligence, and insurance – HOA likely liable for common areas under their responsibilities – Homeowner likely liable for damages inside their unit – Coordination between policies may be required in some cases |

| 7 | File an Insurance Claim: – HOA files claim through master policy if liable – Homeowner files claim through individual policy if liable – Provide documentation (photos, estimates, communication records) |

Are you stuck somewhere along these steps because you’re unsure how to follow them?

Read on for a breakdown of the common causes of water damage and whose responsibility they are, and for more information on you and your HOA’s insurance policy.

If you’d like professionals to do an expert assessment, restore your property to pre-loss conditions, and help you file a claim, then we recommend you get in touch with Lux Restoration.

4 common causes of water damage

As the earlier examples illustrate, it’s crucial to trace the source of the water damage before holding either party responsible. A couple of common sources of water damage are:

1. Plumbing issues

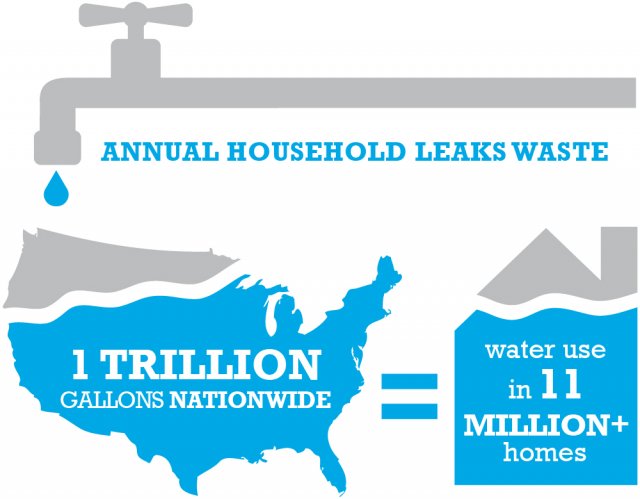

Bust water pipes are a common culprit of water damage. So much so that one in every ten homes have leaky pipes that waste at least 90 gallons of water per day, the EPA found. Reasons for pipes bursting are pressure change, a sudden drop in temperature, or regular wear and tear.

Source: Environmental Protection Agency

Burst pipes within an individual unit often fall under the unit owner’s responsibility. But even if the leaking pipes are located within the unit, the leak might be due to HOA‘s failure to maintain the plumbing system as described under their plumbing responsibilities. In that case, any water damage to both common areas and affected individual units could fall under the association’s liability.

2. Roof leaks

Let’s consult the governing documents of your Homeowners Association. Is the roof of your housing defined as a common element? Then any roof leaks that cause water damage typically fall under HOA’s responsibility.

The CC&Rs should clarify if it’s your HOA’s job to maintain and repair the roof, making them liable for any resulting water intrusion. But suppose the roof leaks due to negligence or lack of maintenance on the unit owner‘s behalf. In that case, the homeowner could be responsible for the water damage and repair costs.

3. Storms and flooding

Locations like Long Island are prone to storm surges and other severe weather events. Between 1980 and 2024, the state of New York experienced 86 weather events of which the costs exceeded $1 billion in costs each. Severe storms accounted for nearly half (48.8%) of the costs, data from the NOAA showed.

The water damage resulting from such an event can be devastating. Because the source of the damage stems from circumstances beyond anyone’s control, the determination of responsibility depends on where the damage occurs.

Source: National Oceanic and Atmospheric Administration (NOAA)

Water damage to common areas and building exteriors are generally the association’s responsibility, while any interior unit damage may still be the responsibility of the individual homeowner, depending on the governing documents and insurance policies in place.

For example, homeowners insurance will often honor claims for weather events that can be categorized as severe, but not if they’re considered natural disasters. To understand your best course of action after a storm causes water damage, it’s best to consult both the CC&Rs and your insurance documents.

4. Broken utilities

Another common source of water damage is a broken appliance or utility, either individually owned or under HOA’s responsibility. Examples are:

- Damaged household appliances like washing machines leaking from faulty hoses or with drainage issues

- HVAC systems that don’t properly drain condensation when cooling air

- Sewage backups like a clogged toilet or sink

In these cases, liability often comes down to where the issue originated – within an individual unit or common area. It also helps to look at any negligence or lack of maintenance that may have contributed to the problem.

Insurance policies and responsibilities

While water damage can be a costly ordeal, the bill won’t necessarily eat into either your or your HOA’s finances. Depending on who’s liable and the water source, the damage can fall under insurance coverage. In fact, water damage is the third-most common insurance claim in the United States, according to consumer research journal ConsumerAffairs. One in sixty insured homes file a water damage claim each year.

Homeowner Associations often (if not always) have a master insurance policy for the common areas and building structures. Individual unit owners are responsible for securing their own homeowners’ or condo insurance policy.

Determining liability takes careful coordination between your HOA‘s master policy and individual homeowners’ insurance providers, plus a clear understanding of the source and location of the water damage as defined by the governing documents.

Master policy

An HOA‘s master policy covers damages to common areas like lobbies, hallways, elevators, and shared amenities like pools or clubhouses. If water damage occurs in the common elements and the source of the water damage falls under the insurance policy, your HOA bears responsibility for repairs and restoration. The HOA board can claim those costs with their insurance company.

But here’s the caveat: HOA insurances sometimes come with deductibles the association pays before insurance coverage kicks in. The HOA board can decide to pass along (a portion of) the deductible to unit owners.

Homeowners’ insurance

If water damage to an individual unit is deemed to be the owner’s responsibility, that unit owner‘s personal homeowners’ or condo insurance policy comes into play.

Homeowners’ insurances cover the interior of an individual unit, including personal belongings and potential liabilities. It’s important to check your insurance papers before filing a claim, because coverage specifics and circumstances depend on the type of policy and insurance company.

Filing the insurance claim

Before you file a claim, all parties involved need to have a clear understanding of responsibility based on the governing documents. Once it’s established where liability lies, either the homeowner or HOA board files an insurance claim for the water damage restoration costs.

If the liability is shared, as would be the case for a severe weather event, file a claim separately for your own unit while your HOA files a claim for the common area.

Document the water damage with photos, repair estimates, and communication records. An insurance adjuster will investigate the claim and approve or deny coverage based on the policy details.

Restoring your home with peace of mind

Whether it’s a leaky pipe or a heavy storm, water can affect your home at any given time. Both HOAs and homeowners have their share of responsibilities in keeping water damage at bay.

When the unfortunate and sometimes inevitable does occur, get in touch with a restoration company. Before restoring your home to its former glory, Lux performs a professional assessment of the water damage and its source to help you determine the responsible party and file a claim.

[Is water destroying your home? Get in touch with us for immediate help. Lux is Long Island’s trusted water damage restoration service with 17+ years of experience in water damage, from fixing flooded basements to restoring storm-damaged roofs.]